The DAX is one of the most widely followed stock indices in Europe and represents one of the most liquid and dynamic markets for systematic trading. Thanks to its volatility and the strong presence of institutional participants, this market lends itself well to a wide range of quantitative strategies.

In this article we will analyze two trading systems applied to the DAX futures contract (FDAX): an intraday breakout strategy and an overnight bias strategy.

Both strategies have been operating successfully for many years out of sample. In other words, they were initially developed using historical data and have continued to perform well in subsequent years on new data that was not used during the development phase. This makes them interesting examples of systematic strategies that exploit persistent structural characteristics of the market.

The DAX Future: One of the Most Interesting Markets for Algorithmic Trading

The DAX index tracks the performance of the largest companies listed on the Frankfurt Stock Exchange and is often used as a benchmark for assessing the health of the German and broader European equity markets.

Active traders typically do not trade the index itself, but rather the DAX futures contract (FDAX), a derivative instrument that replicates the value of the index and allows traders to take both long and short positions efficiently. The futures contract is particularly popular among systematic traders because it combines high liquidity, significant volatility, and relatively low trading costs.

These characteristics make the DAX futures market one of the most widely used instruments for developing quantitative and algorithmic trading strategies, such as the ones we will examine in the following sections.

Intraday Breakout Strategy on the DAX: Trading Logic and Results

The first strategy is an intraday breakout system operating on a 5-minute timeframe. The trading logic is relatively straightforward: the system enters the market when the price breaks above the session high or below the session low, attempting to capture directional moves that often occur after periods of price consolidation.

As is common with many trading systems of this type, several operational filters have been introduced with the goal of improving signal quality and increasing the average trade, one of the most important metrics when evaluating the sustainability of a strategy in live trading.

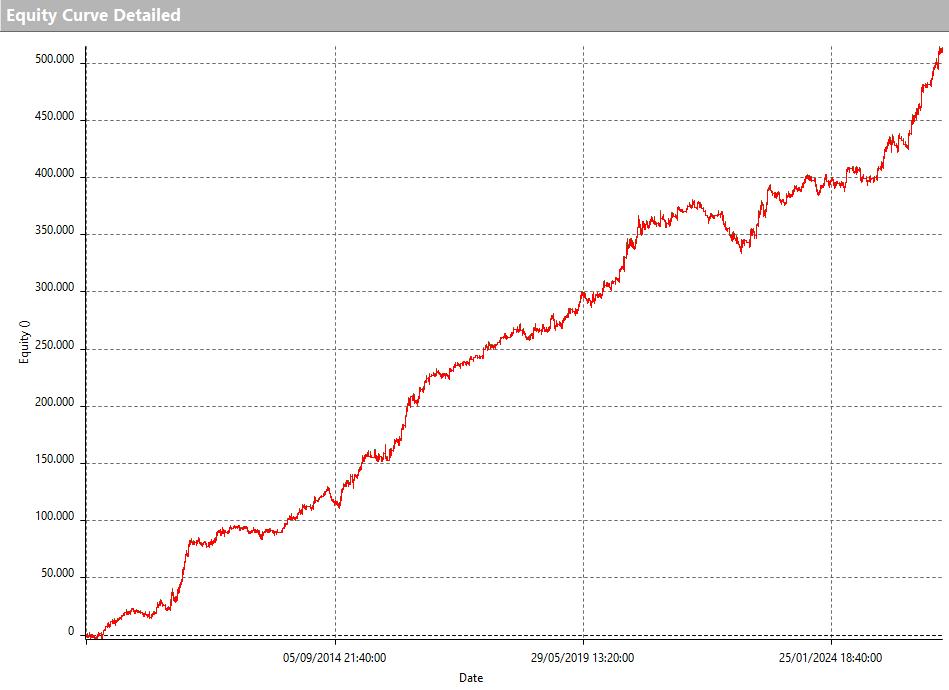

Let’s start by analyzing the performance metrics beginning with the equity curve. The strategy shows a generally upward-sloping and fairly stable growth over the entire historical sample, which runs from 2010 through the last Friday of February 2026. The only particularly challenging period occurred in 2022, a difficult year for global equity markets characterized by significant drawdowns across many financial instruments.

Outside of that period, the strategy maintained good stability. The year 2025 closed with particularly strong performance, and 2026, at least so far, appears to be continuing the same trend, with a very high average trade for the year (around €1,221).

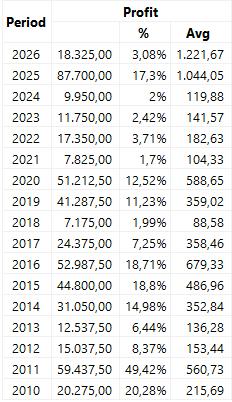

Looking at the Total Trade Analysis, the strategy executed 1,433 trades overall, with an average trade of approximately €357, fairly balanced between long and short positions. This value is large enough to comfortably cover typical live trading costs such as slippage and commissions.

Another interesting aspect is the presence of positive results in most of the analyzed years, despite the drawdown recorded in 2022. This once again confirms how versatile the DAX market can be, offering opportunities both for trend-following and breakout strategies, as well as reversal or bias-based approaches, as we will see in the second part of the article.

For these reasons, many systematic traders consider DAX futures an important component within a diversified portfolio of trading strategies.

Overnight Bias Strategy on the DAX: Exploiting the Overnight Move

The second strategy we will analyze is based on a market bias, meaning a recurring statistical tendency observed in price behavior. In this case, the strategy exploits an overnight bullish bias, a tendency for equity indices to generate positive returns during hours when the European market is closed.

This phenomenon has been documented across several equity markets and represents one of the most studied patterns in quantitative trading. On the DAX as well, a meaningful portion of bullish price movement has historically occurred between the market close and the following session’s open.

The strategy takes advantage of this behavior by entering a long position at 17:45 each day (excluding Fridays) and closing the position at the next session’s open. The system also includes stop-loss and take-profit levels, as well as several filters based on the previous trading day that determine whether or not the trade should be executed.

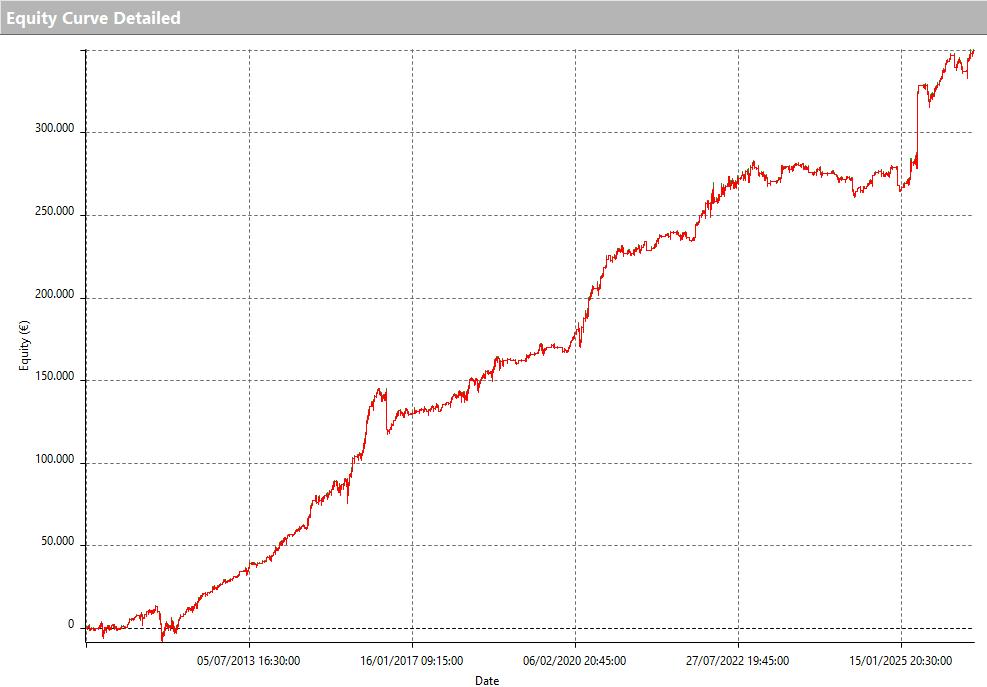

Looking at the performance metrics, the equity curve shows fairly consistent growth across the entire historical period. Some particularly sharp spikes occur during major market events, such as the rebound following the so-called “Liberation Day” in April 2025, when Donald Trump announced new trade tariffs affecting numerous countries, or during the strong recovery that followed the pandemic-driven market crash in 2020.

These trades are clearly outliers relative to the average performance, but they contribute significantly to the overall profitability of the strategy and to the satisfaction of traders who happened to capture them in real time.

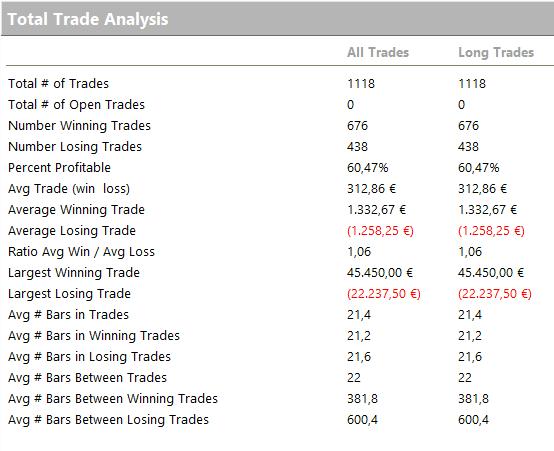

Overall, annual returns are positive in most of the analyzed years. The average trade is slightly lower than that of the breakout strategy discussed earlier, mainly because the average time spent in the market is shorter for a bias-based strategy.

However, the average trade still stands at around €312, which is more than adequate for this market, considering that the DAX futures contract has a value of €25 per point (tick).

Conclusion: Two Different Approaches to Trading the DAX

The two strategies analyzed in this article illustrate how the same market can offer very different types of trading opportunities. On one side we have an intraday breakout strategy designed to capture directional moves during the trading session; on the other, an overnight bias strategy that takes advantage of a recurring statistical tendency observed during overnight hours.

Although the approaches are different, both are built on a systematic framework and aim to exploit structural characteristics of the DAX market.

If you would like to learn more about how trading systems like these are developed, you can book a strategic session with a member of our team using the button in the box below. It’s an opportunity to ask questions, clarify any doubts, and evaluate whether this approach might fit your own trading journey.

That’s all for today, and we’ll see you in the next deep-dive article.